Economists are predicting that between 350,000 and 1-million South Africans could lose their jobs as a result of the Covid-19 pandemic. While it can be difficult to consider the future when faced with retrenchment, withdrawing from your retirement fund, should be your last resort. If you have no other option, try to withdraw only a small portion and increase your contributions once you start working again. You need to ensure you understand and carefully consider the implications of your decision before submitting a withdrawal instruction.

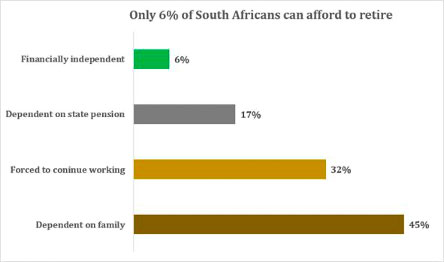

When changing jobs or getting retrenched, 80% of South Africans take their retirement benefits in cash and only 12% transfer to another retirement fund. As a result, only 6% of South Africans will be able to retire comfortably according to the National Treasury and the rest will depend on family, state pension or continue to work.

A survey conducted in 2018 found that South Africans are more willing to put money into a funeral policy or a burial scheme than a pension fund or retirement annuity. This shows that people are able to think about and prioritise their future but for some reason, there is a mental block to retirement. That reason is a behavioural bias called the present bias. The present bias is the tendency to rather settle for a smaller present reward than to wait for a larger future reward, in a trade-off situation. It describes the trend of overvaluing immediate rewards while putting less worth in long-term consequences. The present bias can be used as a measure for self-control, which is a feature related to the prediction of secure life outcomes.

Running out of money will only become a reality in later years

They say ‘Nothing is certain but death and taxes’, I beg for retirement to be added to this list of life’s certainties. But let me go back to address why I’d advise everyone who’s been retrenched to preserve all or a portion of their retirement fund.

To make this easier as possible, I’ll invent an unauthorized retirement nest egg formula and exclude investment returns and salary increases to avoid complexity.

Your retirement fund at retirement = monthly salary multiply by your pension contribution rate multiply by the number of years you contribute to a retirement fund.

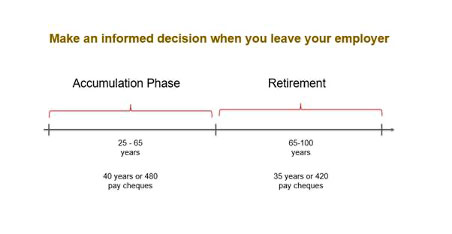

The one factor in this formula that is within your control is the number of years you contribute to a retirement fund (see image below). This is a function of how long you work; which is usually 35 or 40 years for most people. The truth is that every contribution into your pension fund must later become a salary when you are retired. So if you withdraw before retirement, you are stealing from your future self. Once you miss the opportunity to contribute to a retirement fund, it’s gone! You can never make it back. Life expectancy tables indicate that you must expect to earn an income at retirement for at least 27 to 35 years assuming you are of good health.

Our biggest concern as financial advisers is that if you withdraw 100% of your pension fund when you resign or are retrenched or fail to save for retirement, you’ll never get back those years. But at retirement, you’d be expected to have saved enough to sustain you for at least 27 years. The rule of thumb is that your income at retirement must at least be 75% of your last salary. If you were earning R10, 000, you must target to earn R7, 500 (increasing with inflation) until you pass away. According to industry data, only 20% of retirees can afford to earn 75% or more of their final salary before retirement.

We are concerned that a high proportion of people approaching retirement who have not saved enough, expect an unrealistically high level of income from their existing retirement. This unfortunately means that running out of money becomes a reality in later years and, as a result, the likelihood of being able to leave a legacy is severely reduced. To truly break the cycle of poverty and start creating generational wealth, we must prioritise retirement planning.

Speak to a financial adviser before making any decisions about your retirement fund. An adviser will help you to figure out the complexities of your financial situation, and help formalise your plan based on your personal priorities.

Owen Nkomo

Chief Executive Officer

Owen is the founder of Inkunzi Wealth Group and has over 14 years of industry experience. Prior to founding Inkunzi Wealth Group he held various leadership roles at Deutsche Bank, JPMorgan Chase and Citi. He has an Honours degree in Investment Management.